Home Improvement Retail in Q1: A Closer Look at the Trends

The first quarter of this year has brought a mix of encouraging signs and tricky parts for home improvement and furnishing retailers. From evolving consumer habits to the growing influence of online shopping, these companies are finding their way in a market filled with both opportunity and unexpected turns. In this editorial, we take a closer look at how some of the leading names in the industry—Home Depot, Williams-Sonoma, Sleep Number, Lowe’s, and Floor & Decor—performed in Q1, all while considering the broader economic climate that is steering the conversation around retail adjustments and investment prospects.

In a sector where “home is where the heart is,” retailers are tasked with offering a spectrum of products ranging from essential tools and building materials to aesthetic furnishings that complete the living space. Yet, as consumers adapt to the digital age, even traditionally brick-and-mortar outfits are compelled to figure a path through the tangled issues of online commerce, logistical limitations, and fluctuating demand. The good news is that despite these nerve-racking twists and turns, many companies are adapting, albeit at different speeds and with varying degrees of success.

Key Q1 Retail Performance: A Snapshot

To better understand the state of the industry, let’s begin by breaking down the performance and earnings of some notable players. The results, on average, indicate that while revenues have largely met analysts’ expectations, share prices have taken a hit, leaving investors to ponder the implications. Here’s a brief rundown:

- Home Depot: Strong revenue growth of 9.4% year on year but missed EBITDA estimates.

- Williams-Sonoma: Outperformed with a 4.2% revenue increase and delivered the biggest beat on analyst EBITDA – yet trading lower in the market.

- Sleep Number: A rough patch with a 16.4% drop in revenue year on year along with significant misses in earnings per share and EBITDA expectations.

- Lowe’s: Mixed signals with a slight revenue decline but a promising full-year guidance raise.

- Floor & Decor: Achieved modest revenue growth but has guided cautiously for full-year expectations.

While the overall group of home furnishing and improvement retail stocks experienced an average drop of 1.6% in share prices after earnings were announced, it’s clear there are various factors at work—ranging from individual company strategies to broader economic conditions.

Home Depot: Balancing Growth with Market Realities

Home Depot, headquartered in Atlanta, Georgia, is arguably one of the most recognizable names in home improvement retail. With a vast array of products, from power tools to hefty appliances, it has established itself as a one-stop destination for homeowners and professionals alike.

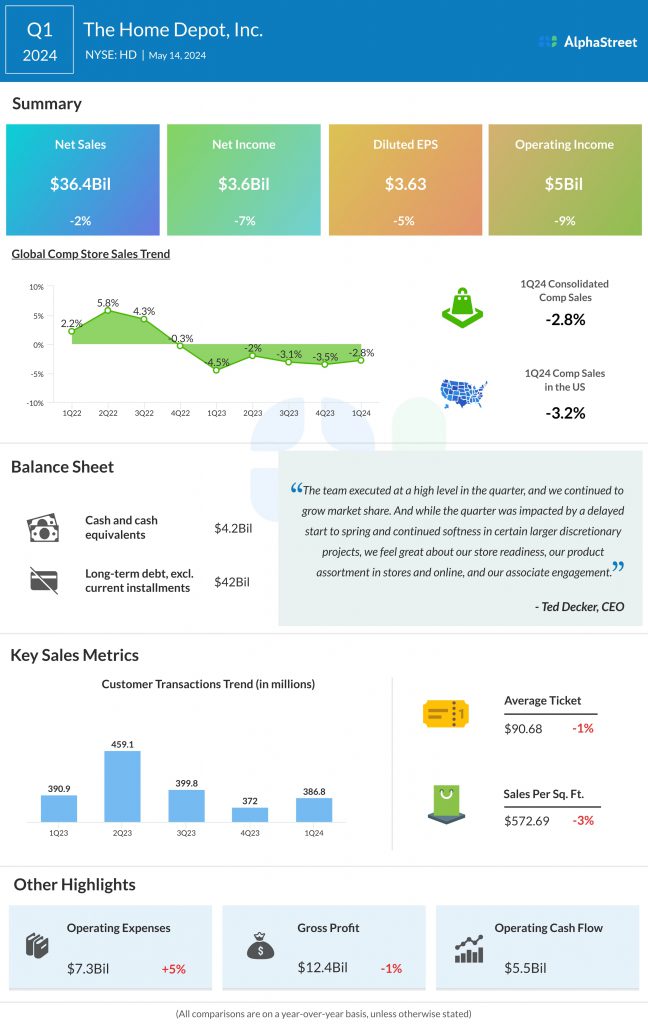

In Q1, Home Depot reported revenues of approximately $39.86 billion—an uplifting 9.4% increase compared to the same quarter last year. This said, the impressive top-line performance was tempered by the fact that the company fell short of analysts’ expectations regarding EBITDA. According to CEO Ted Decker, the steady customer engagement in minor projects and seasonal events was a significant factor in these results.

Despite this progress, the company’s stock fell by 5.9% post-earnings, trading at $356.99 at the time of reporting. Many investors are now weighing growth against the intimidating parts of missing EBITDA benchmarks. For those watching market movements closely, Home Depot continues to be a bellwether for the home improvement sector, yet its current valuation raises questions on how to best approach investing in this kind of retail environment.

Performance Details: Home Depot at a Glance

| Metric | Q1 Performance | Analysts’ Expectations |

|---|---|---|

| Revenue | $39.86 billion (up 9.4% YoY) | In-line |

| EBITDA | Fell short | Above the mark |

| Stock Movement | Down 5.9% | — |

For investors, the key takeaway from Home Depot’s earnings is that, despite healthy revenue growth, the turbulent bits related to operating margins invite a careful study into the future trajectory of the company’s performance. The stock’s underperformance post-reporting suggests that while consumers remain engaged at the grassroots level, the market is also cautious about potential headwinds.

Williams-Sonoma: A Beacon of Optimism in a Competitive Field

Williams-Sonoma stands out as a specialty retailer that entered the market originally with a niche focus on French cookware. Over the years, however, it has broadened its scope to include a host of upscale kitchenware, home goods, and furniture. The evolving product lineup has helped the company carve out a premium positioning in the competitive home furnishings landscape.

In Q1, the retailer recorded revenues of $1.73 billion, showcasing a favorable 4.2% increase on a year-to-year basis. More notably, Williams-Sonoma outpaced many peers by outperforming analysts’ expectations by 4%, and it stood out with the biggest beat on EBITDA estimates among similar companies.

It is interesting to note that despite these encouraging numbers, the market reaction has been somewhat underwhelming. The Williams-Sonoma stock is down 2.1% since reporting, trading at around $164.10. This disconnect between strong performance metrics and stock price movement raises some intriguing questions about short-term market sentiment, where investors might be looking at broader economic factors or awaiting further market clarity before driving up the stock valuations.

Analyzing Williams-Sonoma’s Performance

- Revenue Growth: Consistent results with a 4.2% increase, indicating stable customer demand for upscale home goods.

- EBITDA Beat: The company’s ability to outperform estimates hints at strong operational control and efficient cost management.

- Market Reaction: Despite stellar earnings, the stock price dipped slightly, a reflection of cautious market behavior amid wider economic uncertainty.

This scenario emphasizes the tricky parts of connecting quarterly performance with immediate investor sentiment. In many cases, earnings are only one stamp in a longer chain of market expectations that include economic policy changes, consumer trends, and competitive dynamics. For those with a longer investment horizon, Williams-Sonoma remains an attractive proposition, yet trends over subsequent quarters will be key in determining whether the market will finally recognize its positive fundamentals.

Sleep Number: Facing a Chilly Q1

Sleep Number, known for its innovative adjustable mattresses and streamlined bedding solutions, encountered an off-putting and challenging quarter in Q1. The company, which focuses on delivering personalized sleep experiences, reported revenues of $393.3 million—a steep 16.4% drop compared to last year. Not only did these numbers fall short of what analysts had hoped for, but the company also missed important milestones on EBITDA and earnings per share.

The significant miss in performance has translated into a stock decline of 10.8%, with Sleep Number trading at $6.95 at the time of reporting. Such a sharp downturn underscores the nerve-racking reality for a firm that might be struggling to keep pace with both consumer expectations and the fast-evolving competitive landscape.

Understanding the Challenges at Sleep Number

- Revenue Slump: A drop of over 16% YoY indicates that consumer demand has softened, likely due to external factors or internal operational hurdles.

- EBITDA and EPS Miss: Falling short on these key metrics highlights the company’s struggle to maintain profitability in a competitive market space.

- Investor Sentiment: A 10.8% dip in stock price reflects broader market apprehension and the caution with which investors are approaching the firm.

The cautious nature of the current economic environment combined with the off-putting quarterly performance has left many industry watchers wondering if Sleep Number can quickly rebound. Continued innovation, restructuring, or sharper strategic focus may be necessary to tackle these challenging times head-on. As the market digests these results, stakeholders are likely to keep a keen eye on how the management plans to steer through the upcoming quarters.

Lowe’s: Navigating a Mixed Q1 With Cautious Optimism

Lowe’s, another stalwart in the home improvement arena, delivered a mixed bag of results in Q1. The company, which started its journey as a humble hardware store in North Carolina, now boasts the profile of a major retail enterprise. In the first quarter, Lowe’s reported revenues of $20.93 billion—a slight 2% decrease compared to the previous year. This modest contraction in top-line revenue was in line with analysts’ expectations, guiding the company into a cautious path for the rest of the year.

On the margin front, Lowe’s managed to nail a narrow beat on the gross margin estimates. Moreover, the company raised its full-year revenue guidance—the highest among its peers—suggesting that management is confident in its ability to recover and adapt. However, the stock has reacted negatively in the short term, down 6.2% since the earnings announcement, trading at $216.59.

Key Takeaways from Lowe’s Performance

- Steady Revenue Guidance: Despite a minor revenue decline, the upward full-year guidance offers hope and indicates strong management optimism.

- Gross Margin Beat: A slight beat in margin estimates can hint at operational efficiencies that might boost profitability over time.

- Mixed Market Reaction: The drop in stock price suggests that while investors appreciate the raised guidance, they remain cautious about the near-term slowdown.

Lowe’s performance in Q1 is a classic example of a company working through mixed signals in an evolving economic backdrop. By raising future guidance, Lowe’s is betting on the recovery and continued consumer spending easing back into the improvement market. For market watchers, these results are a reminder that the short-term dips in stock values don’t always capture the full picture of long-term potential.

Floor & Decor: Building Appeal in a Dynamic Market

Operating large, warehouse-style specialty stores focusing on hard flooring surfaces like tiles, hardwood, and stone, Floor & Decor has positioned itself uniquely in the home improvement industry. Its product focus has attracted a niche customer base that is passionate about upgrading the look of their living spaces.

In Q1, the company reported revenues of $1.16 billion, marking a 5.8% increase compared to the same period last year. While these numbers met the analysts’ expectations for revenue, the company fell into the trap of not meeting full-year revenue and EBITDA guidance estimates. This cautious projection has raised concerns among some investors about the scalability and consistency of its performance.

Detailed Performance Snapshot for Floor & Decor

- Revenue Growth: A healthy 5.8% increase signals growing consumer demand for aesthetic home improvements.

- Guidance Concerns: The shortfall in full-year revenue and EBITDA guidance indicates that there might be underlying factors that could hinder future growth.

- Stock Movement: Interestingly, while the guidance leaves room for apprehension, the stock is up 8.6% since the earnings release, currently trading at $78.53.

The performance of Floor & Decor presents a complex picture. On one side, steady revenue growth presents a promising indicator for continuing consumer interest in home décor and improvement. On the other, the company’s cautious full-year projections remind investors of the unpredictable twists and turns that come with market expectations and economic pressures.

Transitioning to Digital: The Evolution of Home Improvement Retail

One of the most compelling shifts that the home improvement retail sector has had to manage is the move to digital commerce. Decades ago, the industry was largely viewed as immune to the rapid expansion of e-commerce due to the tangible, often bulky nature of its products. Shipping a sofa or a lawn mower was considered too logistically challenging. However, retail pipelines have changed drastically, with companies now offering robust online options that cater to a tech-savvy generation.

This transition reflects a broader evolution where companies are not just focusing on physical store performance but also on making a strong digital presence. The market is currently loaded with issues such as ensuring a seamless customer experience online, managing complicated logistical pieces, and competing with pure-play e-commerce giants.

Challenges of the Digital Shift

- Logistical Hurdles: The transportation and delivery of heavy or oversized products still present some twisted turns that need careful strategic planning.

- Customer Engagement: Moving online requires digital tools that can maintain the high level of customer interaction expected in physical stores.

- Operational Integration: Companies must now figure a path to integrate digital sales channels with traditional retailing to balance revenue streams effectively.

Retailers like Home Depot and Lowe’s have invested heavily in online platforms, developing user-friendly websites and robust supply-chain systems to support these changes. These initiatives not only help boost sales but also position the companies favourably for a future where the digital realm plays an essential role in the overall shopping experience. The experiences from Q1 underscore not only the progress made but also the challenging bits that remain as these companies continue to adapt.

Market Dynamics: Inflation, Interest Rates, and Economic Policy Changes

The broader economic stage is equally instrumental in shaping the narrative for home improvement retailers. The strategic decisions made by the Federal Reserve in the past couple of years have significantly influenced market behavior. Following a series of interest rate hikes during 2022 and 2023 aimed at cooling post-pandemic inflation, the recent rate cuts signal a promising outlook for economic stability in 2024.

Many experts view these policy shifts as a move towards a soft landing, where inflation pressures are eased without plunging the economy into a full-blown slump. In simple terms, the economy is carefully finding its way through the overwhelming parts of post-pandemic recovery, and this stability has had a noticeable effect on stock market performance. With recent record surges in major indices and optimistic signals from policy adjustments, investors continue to watch closely how any potential corporate tax changes or tariffs may weigh in on the market next year.

Impact of Economic Policy on Retail Performance

- Interest Rate Adjustments: Recent cuts, such as a 0.5% reduction in September 2024 and a 0.25% cut in November 2024, are expected to ease financing costs for businesses and consumers alike.

- Inflation Control: Cooling inflation is a key factor that is creating a more predictable environment for retailers, helping stabilize costs and consumer spending.

- Policy Uncertainty: Despite these positive signs, potential adjustments in corporate tax laws and new tariffs remain off-putting concerns that could influence investment decisions in 2025.

This layered economic context feeds back into the performance of home improvement retailers. Companies that have solid fundamentals but are also versatile enough to manage these economic twists and turns will likely stand out in an uncertain future. For investors, watching how these market dynamics influence earnings is crucial for making well-informed decisions.

Investor Outlook: Balancing Short-Term Movements with Long-Term Strategy

The Q1 earnings cycle for home furnishing and improvement retailers reveals both promising trends and areas laden with challenges. Many investors are now faced with the task of filtering through a barrage of quarterly figures, market dips, and strategic guidance to pinpoint which companies are best positioned for long-term success.

In the short term, stocks like Home Depot and Lowe’s experienced declines that might worry those with a keen eye on quarterly performance. However, deeper analysis shows that raised future guidance and consistent revenue growth are factors that can help mitigate some of these concerns for long-term investors. At the same time, companies like Williams-Sonoma have proven resilient with strong EBITDA performance, even if the market reaction has been a bit muted.

Strategies for Evaluating Retail Investments

- Examine Revenue Trends: Look beyond quarterly fluctuations and focus on consistent growth patterns over several periods.

- Focus on Operational Efficiency: Companies that manage to beat margin expectations often reveal hidden strengths in cost management and process optimization.

- Assess Future Guidance: Raised guidance, as seen with Lowe’s, is a critical indicator of management’s confidence despite short-term setbacks.

- Monitor Macroeconomic Indicators: Changes in interest rates, inflation, and government policies will continue to impact consumer behavior and retailer performance.

In summary, while short-term headwinds have caused share price drops in several key players, the underlying fundamentals and strategic initiatives embedded in these companies point to potential for recovery and growth over the coming quarters. Investors who are comfortable filtering through the confusing bits of quarterly performance and economic indicators may find promising opportunities in the sector.

Looking Ahead: Future Prospects for Home Improvement Retail

As we move further into 2024 and beyond, the home furnishing and improvement retail sector is positioned at a crossroads. The dual pressures of adapting to a digital-first commerce model and managing economic shifts mean that companies must constantly refine their game plans. Whether it’s rethinking supply-chain management, investing in online platforms, or adjusting operational strategies, the path ahead is both challenging and ripe with opportunity.

For example, companies like Home Depot and Lowe’s are stepping up their digital transformation efforts, while Floor & Decor focuses on niche product lines that attract dedicated consumer segments. The companies that succeed will most likely be those that not only pace the immediate shifts in consumer preferences but also nurture sustainable, long-term business models that adapt fluidly to market changes.

Future Trends to Watch

- Enhanced Online Integration: Expect more retailers to invest in smoother online shopping experiences, from virtual product tours to live customer support.

- Supply-Chain Innovations: The push for quicker delivery and efficient logistics will be a focal point as companies look to overcome logistical hurdles and reduce costs.

- Consumer-Centric Innovations: Personalized products, customization options, and enhanced customer engagement will continue to drive market differentiation.

- Sustainability Practices: As consumer awareness about environmental issues grows, investments in sustainable products and ethical practices may become key differentiators.

Retailers aiming to secure a competitive edge in the upcoming quarters will need to be agile in managing these subtle details while remaining resilient amid the more intimidating market factors. Together, these trends paint a picture of an industry that is evolving—and quickly at that—as it strives to balance tradition with modernity.

Conclusion: Embracing the Future with a Measured Perspective

In conclusion, the Q1 earnings results for home improvement and furnishings retailers highlight a landscape of both cautious optimism and challenging bits. On one end, companies have delivered robust revenue figures and raised future guidance, underscoring their potential to pull ahead in the long run. On the other, the stock market’s immediate reaction reminds us that investors are sensitive to every twist and turn amid economic uncertainty.

For both industry insiders and everyday investors, the messages from Q1 are clear: continue to work through the evolving marketplace by focusing on strategic initiatives, refining digital capabilities, and keeping a close eye on macroeconomic signals. Whether it’s the steady performance of a giant like Home Depot or the resilient beats from specialty players like Williams-Sonoma, the evolving narrative of this sector tells us that adaptability and strategic clarity are the must-have traits for navigating a future that is as promising as it is unpredictable.

The road ahead will likely be filled with a mix of small distinctions and subtle parts of success that can only be uncovered through careful analysis and until-the-last-minute market observation. Investors and industry watchers alike would do well to remember that quarterly numbers are just one piece of the larger puzzle: long-term growth is often built on the foundation of consistent operational improvements and strategic foresight.

Whether you are a seasoned investor or just starting to build a diversified portfolio, staying informed about these evolving trends and understanding the finer points of each company’s strategy is essential. As we see economic policies continue to shift and companies get creative in their digital endeavors, the home improvement retail sector stands out as a fascinating case study in balancing traditional business strengths with modern-day innovations.

In weighing these varied perspectives, it becomes clear that the future holds both challenges and substantial rewards. The companies that can best manage the confusing bits of digital integration, supply-chain refinement, and economic policy changes are those that will likely come out ahead as we move forward into a new chapter of retail evolution.

Key Insights for Investors

| Aspect | Insight |

|---|---|

| Revenue Trends | Steady performance can mask underlying market uncertainties—an in-depth look is necessary for true evaluation. |

| Operational Margins | Meeting or beating margin estimates is a good sign of effective management, even if short-term market sentiment is negative. |

| Digital Integration | Investments in e-commerce platforms are essential as consumer shopping behaviors continue to evolve. |

| Economic Outlook | Policy changes and interest rate adjustments remain key indicators of future consumer spending and retail performance. |

Ultimately, the art of investing in home improvement retail stocks in today’s environment is about balancing short-term market swings with a long-term vision. The companies that consistently invest in their operational strengths, while not shying away from recalibrating their strategies to meet new demands, are the ones that stand a better chance at weathering the unpredictable climate of market conditions.

As we wrap up this deep dive into the Q1 performance of major home improvement and furnishing retailers, it’s worth reiterating that while some companies are navigating the tricky parts of current market conditions better than others, the overall outlook for the industry remains cautiously optimistic. From noteworthy beats by Williams-Sonoma to the sobering challenges faced by Sleep Number, the diversity in performance reminds investors to keep an open, yet watchful, perspective.

In the end, for those looking to invest in winners with robust fundamentals, keeping an eye on the home improvement retail sector offers both opportunities and valuable lessons. Whether you’re reexamining your portfolio or just taking the time to get into the finer points of market trends, there’s plenty to learn from the way these companies—each with their unique strengths and challenges—are adapting to a fast-changing business landscape.

There is no one-size-fits-all answer in the realm of investing, but by clearly evaluating revenue trends, operational efficiencies, and the broader economic context, investors can better figure a path through the nerve-racking fluctuations of the market. This measured perspective, backed by a strategic understanding of both immediate and long-range trends, is the cornerstone to building a resilient and rewarding investment portfolio.

Looking ahead, the onus is on both company leadership and their stakeholders to work through the nuanced elements of business strategy and market dynamics. With new digital enhancements, evolving consumer expectations, and global economic shifts on the horizon, the home improvement retail landscape is set for a period of transformation—one that invites both caution and opportunity.

In closing, keep a watchful eye on the small distinctions that can make or break success in this sector, and remain flexible in the face of changing conditions. As we continue to see the interplay between traditional retail strengths and modern innovations, it is clear that the companies best equipped to manage these tangled issues will ultimately lead the pack. Whether you’re an industry veteran or a newcomer, there is wisdom to be gleaned from each quarterly report, and the journey of these retailers is a testament to the art of balancing tradition with the necessary drive for innovation.

Originally Post From https://stockstory.org/us/stocks/nyse/hd/news/earnings/q1-rundown-home-depot-nysehd-vs-other-home-furnishing-and-improvement-retail-stocks

Read more about this topic at

Earnings Rundown

Earnings Calendar